8th May 2026

Our blogs often focus on the sex and violence of investment trust governance, small-cap equities and other high-octane markets, but it’s worth remembering that a good chunk of our Funds are invested in a far less glamorous asset class – Bonds (Global Opportunities less so). Indeed, Vanbrugh as a constituent of the IA Mixed Investment 20-60% Shares sector must have a minimum of 30% allocated to fixed income and cash. Different bonds can play different roles at different times in a multi-asset portfolio whether that be as a provider of ballast, a generator of income, a total return play or a diversifier of equity risk. However, as with any other asset class it’s important to remember that the risk-return and correlation characteristics of bonds are not static properties but instead wax and wane over time.

So, where are we now? Following the great reset of 2022, sovereign bond yields remain relatively high, particularly in the UK where inflation concerns, the premium associated with political risk and the demise of traditional defined benefit pension scheme buyers have driven the yield on the 10-year gilt to 5.1%. Despite clear macro risks, credit spreads within both investment grade and high yield trade at historically tight levels reflective perhaps of the appeal of high all in yields.

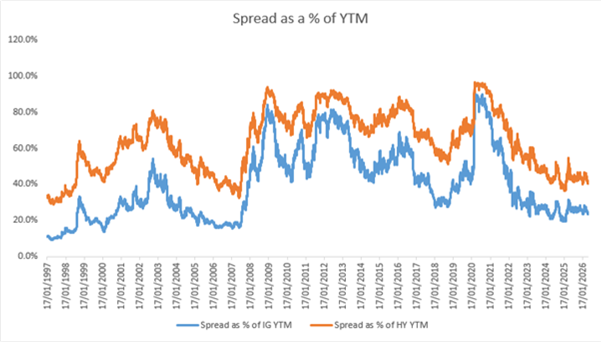

As with any other asset class, we are constantly looking for the best relative value within fixed income. Currently we have a clear preference for government bonds over corporates. Some measures we look at to inform this view include the proportion of a corporate bond’s yield to maturity (YTM) that is made up of spread versus the risk-free rate. As the chart below demonstrates, the combination of relatively high government bond yields and tight credit spreads means this is at a multi-decade low.

Source: Hawksmoor Investment Management January1997 – January 2026

Spread breakevens which measure the extent to which credit spreads can widen before an investor is better off in an equivalent duration sovereign are also at very low levels. The sterling investment grade bond index currently trades with a spread of around 90bps and a spread duration of 6 years, meaning that if spreads widen by 15bps or more your higher risk corporate will underperform your equivalent government bond. Margin of safety is scant. In short, we strongly believe that credit spreads at the index level currently fail to adequately compensate investors for the additional default, liquidity and mark to market risk associated with corporate bonds.

Valuation dispersion within credit markets has narrowed somewhat in the past year, but remains wide enough for nimble active managers to exploit enabling them to deliver YTMs handsomely above that of the index. Away from vanilla corporate bonds we continue to see opportunities in securitised credit where the complexity premium associated with the likes of RMBS and CLOs drive higher risk adjusted yields and where floating rate coupons bring a different and useful diversifying dynamic to a fixed income portfolio. Emerging market debt also offers attractive prospective returns with our favoured manager adopting a very active approach and effectively hedging out the US Treasury duration that comes with external EM bonds.

Talking of duration, yield curves have steepened in the past few years but with inflation volatility elevated and concerns regarding fiscal largesse and a wave of issuance never far from the surface, we are minded to stay away from the long end of the bond market. We try not to do macro (although that’s nigh on impossible when it comes to rates) but recognise there is a scenario and historic precedent for curves to steepen considerably from here. We also see a risk that the positive equity-bond correlation that characterised 2022 plays out again, negating fixed income’s potential as a risk-off hedge. As such our government bond exposure is focussed on shorter dated, less rate sensitive areas where decent starting yields offer the prospects of positive real returns and far less downside in a rising yield environment.

The duration of the fixed income component of our Funds is also informed by the rate sensitivity we have elsewhere in the portfolio. The relationship between gold and real rates has broken down of late but we continue to view the yellow metal as the ultimate long duration asset. Unlike pieces of paper issued by Uncle Sam or the UK government gold is no one’s liability and we have much greater faith in gold’s ability to act as a diversifier to equity risk than we do long dated bonds issued by indebted governments – as well as believing it can generate positive real returns. We also have significant exposure to infrastructure and renewables via investment trusts which have inherent rate sensitivity owing to the discounted cash flow methodology used to value their portfolios and the fact that many investors value these investments on a comparable yield basis. Yielding between 7% and 11% and paying often progressive dividends from defensive underlying assets with low counterparty risk, we’d rather concentrate our duration risk here.

Summing up, we are currently defensively positioned within fixed income with both credit risk and interest rate risk at relatively low levels. Indeed, of Vanbrugh’s rated bond exposure 77% is currently in AAA-A rated bonds. The duration of the fixed income component is just 3.8 years. We accept that in a deflationary risk off episode in which yields fall our fixed income might offer less of a portfolio hedge than some, but we’re comfortable with this, confident that the exposure will hold up well in a wider range of scenarios and pay us a positive real return in the meantime. As ever we remain alive to shifts in relative value and are nimble enough to quickly move our fixed income exposure as the opportunity set changes. We’ll let you know if things get more exciting.

Ben Mackie – Senior Fund Manager

Subscribe to receive our latest commentary and insights straight to your inbox.

For professional advisers only. This document is issued by Hawksmoor Fund Managers which is a trading name of Hawksmoor Investment Management (“Hawksmoor”), the investment manager of the MI Hawksmoor Distribution Fund (“Fund”). Hawksmoor is authorised and regulated by the Financial Conduct Authority. Hawksmoor’s registered office is 2nd Floor Stratus House, Emperor Way, Exeter Business Park, Exeter, Devon EX1 3QS. Company Number: 6307442. The Fund’s Authorised Corporate Director, Apex Fundrock Ltd (“Apex Fundrock”) is also authorised and regulated by the Financial Conduct Authority. This document does not constitute an offer or invitation to any person, nor should its content be interpreted as investment or tax advice for which you should consult your financial adviser and/or accountant. The information and opinions it contain have been compiled or arrived at from sources believed to be reliable at the time and are given in good faith, but no representation is made as to their accuracy, completeness or correctness. Hawksmoor, its directors, officers, employees and their associates may have a holding in the Fund. Any opinion expressed in this document, whether in general or both on the performance of individual securities and in a wider economic context, represents the views of Hawksmoor at the time of preparation and may be subject to change. Past performance is not a guide to future performance. The value of an investment and any income from it can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you originally invested. FPC26704.